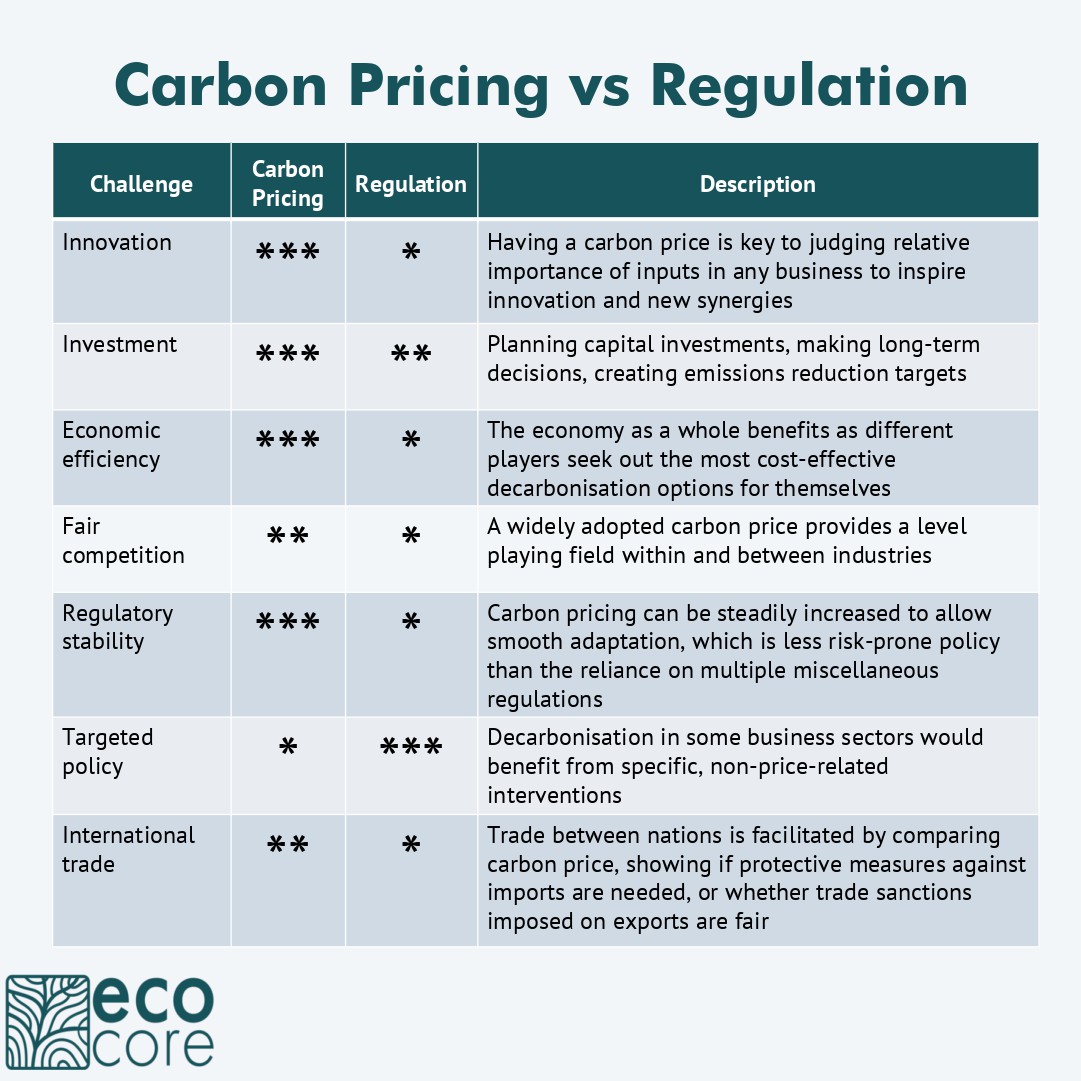

The de facto industry standard for reporting CO2 is the GHG Protocol, with its omnipresent Scope 3 emissions. See the table below for definitions. Scopes 1 and 2 emissions are easily measured and targeted, but Scope 3 emissions include indirect emissions occurring in a company’s supply chain, both upstream and downstream.

| Type | Standards or Governance | Definition |

|---|---|---|

| Scope 1 | WRI/WBCSD GHG Protocol | from direct result of burning fossil fuels, e.g. when transporting goods in a lorry that runs on diesel |

| Scope 2 | WRI/WBCSD GHG Protocol | not directly from the company or organisation, but caused by an energy provider burning fossil fuels to provide, for example, energy that the company buys |

| Scope 3 | WRI/WBCSD GHG Protocol | all other emissions that result from the company or organisation’s activities but aren’t in scope 1 or 2, e.g. an oil company includes emissions from combustion of the oil it sells in its own scope 3, although they are also another company’s scope 1 emissions. Many sub-types. |

| Scope 4 / Avoided | ISO, also CDP | prevented or reduced due to a company’s products, services, or activities. Addresses the positive impact of a company’s products or services, e.g. bike-sharing company counts avoided emissions from car travel |

| Scope 5 / Removed | Proposed | physical removal of atmospheric CO2 through human action |

| Facilitated Emissions | SBTi, CDP, TCFD, PCAF | mainly in the financial sector (banks, asset managers, and insurers) who facilitate emissions through lending, investment & underwriting, particularly fossil fuel industry. See also scope 3.15 |

| Upstream Emissions | Implied | Occur before the company’s operations, including capital, energy, transportation, waste, purchases, leasing |

| Downstream Emissions | Implied | Occur after a company’s operations, linked to how a company’s products are distributed, used, and disposed of |

This reporting protocol enables the company to identify decarbonisation challenges across the whole industry sector it is a part of. What it doesn’t do though is define exactly what the carbon emissions associated with a particular product or service are. In other words, it’s no practical help when a purchaser is attempting to find the lowest emissions items to buy.

To have an idea of the CO2 emissions associated with particular goods or services, the interested party must carry out a full lifecycle assessment of the product to determine cradle-to-grave emissions.

EcoCore’s concept of carbon accounts doesn’t create such a division of labour. Products and services in an economy working within the carbon accounts framework would be sold with an associated carbon price reflecting only the upstream and direct CO2 emissions. So the carbon price of the product is the carbon footprint of the sold item as it goes over the counter.

The carbon footprint of the company takes on an entirely different meaning. Under the carbon accounts policy, it would simply be all the company’s emissions that weren’t explicitly tied to production of a unit, i.e. property management, executive travel etc. It would be of no interest to anyone outside the company, and those inside the company would have to work out the best way to cover the carbon ‘expenditure’, most obviously by adding it on to the carbon price of each product sold.

Voluntary carbon markets

Markets where companies and individuals purchase carbon credits on a voluntary basis to offset their emissions.

Compliance carbon markets

Regulated markets where companies must adhere to legally mandated carbon reduction requirements.

Facilitated Emissions

Banks are divided over how to account for carbon emissions linked to their capital markets business. Some propose that 100% would be attributed to them rather than to investors who buy the financial instruments. Others object. An industry-wide methodology was due to be announced in late 2022. A proportion of the emissions was to be booked by each bank. Most banks are yet to reflect the emissions associated with the deals they do in their targets, making it hard to track their progress towards pledges to reach net-zero emissions by 2050. As of writing in view of President Trump’s climate policy reversals, this is likely to stay the same or be dropped entirely.

Sources

ShareAction, a responsible investment NGO.

The US EPA https://www.epa.gov/climateleadership/scope-1-and-scope-2-inventory-guidance

Acronyms Used

- CDP – Carbon Disclosure Project

- PCAF – Partnership for Carbon Accounting Financials

- SBTi – Science-based Targets Initiative

- TCFD – Task Force on Climate-related Financial Disclosures

- WBCSD – World Business Council for Sustainable Development

- WRI – World Resources Institute

More in this Series

The voluntary carbon markets are estimated to have a turnover in 2022 in the order of US$ 2 billion. Current estimates…

Carbon pricing: what is it? Essentially it is just information about money – the price signal, which you need if you…

A carbon price is the key factor that business, industry and the economy need for a swift and efficient energy transition.…

Despite decades of carbon trading, CO2 emissions continue to rise, and it seems little can improve the carbon markets. The impact…

EcoCore’s hypothesis is that our Carbon Accounts framework would create the strongest carbon pricing signal above any other approach to drive…